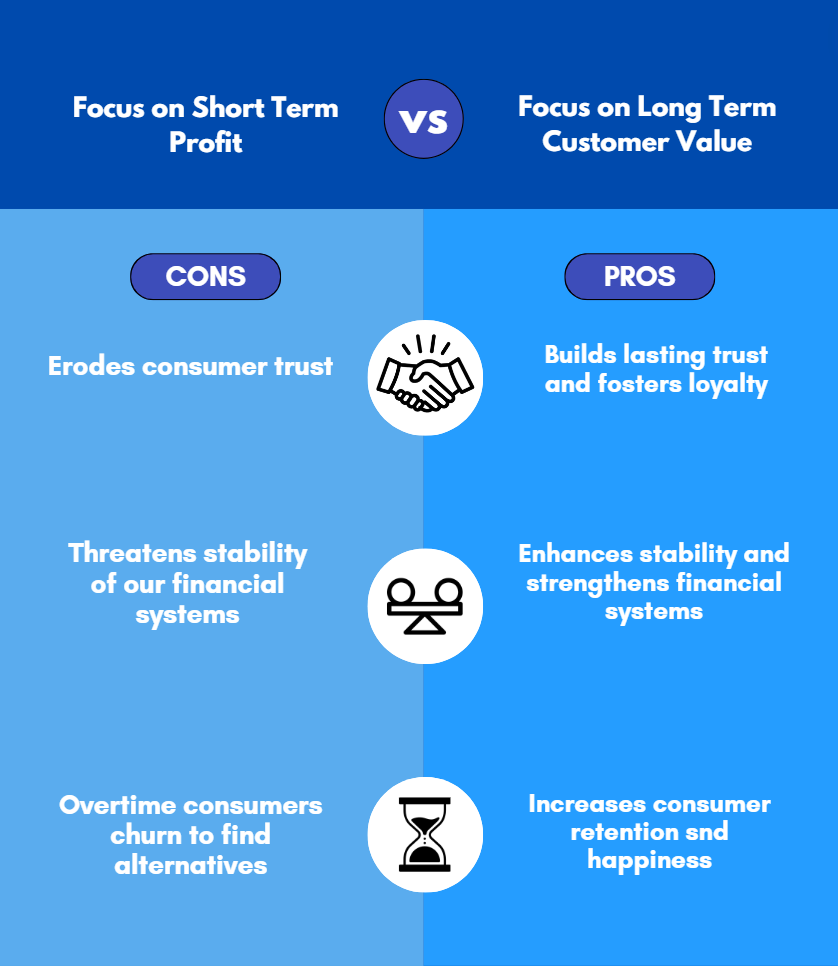

In today’s financial landscape, a troubling trend has emerged: financial institutions increasingly prioritize short-term profits over genuine customer value. This relentless pursuit of profit has overshadowed the commitment to serving customers. Jeff Bezos in his annual letters to shareholders since 1997 has continued to iterate that focusing on the customer to create customer value will in the long term create shareholder value. His unwavering commitment to customer satisfaction has solidified Amazon’s position as a leader in the global marketplace. Yet, when we look at the current financial and crypto ecosystems, the focus on short-term gains is eroding consumer trust and threatening the stability of our financial systems.

The Profit-First Mentality

At the core of this issue lies a profit-first mentality that has seeped into both traditional financial institutions and crypto exchanges. While profitability is essential for business survival and growth, an extreme focus on short-term gains and shareholder value has dangerously neglected customer interests.

Traditional Financial Institutions

Banks and other financial institutions have long been criticized for putting profits ahead of customer welfare. This is evident in several predatory practices that exploit rather than serve consumers:

- Predatory Lending Practices: Payday loans with exorbitant interest rates, and credit cards with steep APRs, take advantage of vulnerable individuals, prioritizing short-term profits over the long-term financial health of their customers.

- Complex Financial Products: Banks create and push complex financial instruments that generate high fees, often at the expense of customer understanding and benefit.

- Inadequate Customer Service: Cost-cutting measures reduce customer support, making it difficult for customers to resolve issues or receive personalized advice.

- Artificial Friction: Banks create unnecessary barriers to prevent customers from canceling products, such as requiring balance protection plans to be canceled via fax — a method most people no longer use. These tactics are designed to retain customers through inconvenience rather than offering genuine value.

Crypto Exchanges

Cryptocurrency was born from a vision of decentralization and financial empowerment, but many crypto exchanges have fallen into the same traps as traditional financial institutions:

- High Trading Fees: Some exchanges charge exorbitant fees, especially during peak trading times, prioritizing profit over accessibility.

- Artificial Withdrawal Barriers: Many exchanges impose high withdrawal fees, often calculated as a percentage of the withdrawal amount, discouraging users from moving their funds off the platform.

- Hidden Fees and Spreads: Some exchanges obscure the true cost of transactions by not showing the spread prices or hiding fees within the pricing. This lack of transparency makes it difficult for users to understand the real cost of their trades.

- Aggressive Marketing of High-Risk Products: Promoting highly leveraged trading options to inexperienced users, leading to significant potential losses.

Telecom Industry: A Parallel in Non-Financial Sectors

While not directly a financial institution, the telecom industry has long operated in a similar fashion, leveraging its near-monopoly status to engage in underhanded tactics designed to maximize profits at the expense of customer clarity and fairness:

- Complex Billing Plans: Cell phone bills and phone plans have been deliberately crafted to confuse customers, with complex pricing structures that often lead to overcharges.

- Confusing Phone Bills: Phone bills were deliberately designed to be confusing, making it difficult for customers to pinpoint where overages occurred.

- Creative Overcharges: Telecom companies invented ways to increase revenue, such as limiting text messages on certain plans and charging up to $0.15 per text message — an excessive fee that generated billions in profits. These practices were intentionally designed to catch customers off guard and capitalize on their lack of understanding.

The Cost of Misaligned Incentives

The focus on short-term profits and shareholder value comes at a significant cost:

- Erosion of Trust: Consumers increasingly view financial institutions and exchanges as adversaries rather than partners in their financial journey.

- Financial Instability: Risky practices driven by profit motives can lead to market instabilities and economic downturns.

- Widening Wealth Gap: As institutions prioritize wealthy clients and high-volume traders, average consumers are left with subpar services and fewer opportunities for financial growth.

- Regulatory Backlash: The focus on profits over consumer protection invites stricter regulations, which can stifle innovation and increase costs for all participants.

The Model of Integrity and Fair Pricing

Contrast this with companies like Cost Plus Drugs by Mark Cuban and Costco. These companies have built incredibly successful businesses on principles of fairness and transparency in pricing, standing in stark contrast to the profit-maximizing approaches of many financial institutions.

Cost Plus Drugs: A Case Study in Ethical Pricing

Cost Plus Drugs, founded by Mark Cuban, has taken a bold stand against the pharmaceutical industry’s long-standing practices of inflated pricing and opaque cost structures. In a sector where consumers often struggle to understand why their medications cost so much, Cost Plus Drugs offers a refreshingly transparent approach. The company operates on a simple yet revolutionary model: a 15% markup on the wholesale price of drugs, plus shipping. There are no hidden fees, no convoluted pricing tiers, and no confusing insurance hoops to jump through — just clear, straightforward pricing.

This transparency is not just a marketing strategy; it’s a fundamental shift in how the pharmaceutical industry can — and should — operate. By stripping away the layers of obfuscation that have long shrouded drug pricing, Cost Plus Drugs empowers consumers to see exactly what they are paying for. This model not only reduces costs for patients but also challenges the status quo, forcing other companies in the industry to reevaluate their pricing strategies. In an era where medical expenses can be crippling, the ethical pricing model of Cost Plus Drugs provides a blueprint for how businesses can prioritize consumer value without sacrificing profitability.

The Costco Model: Integrity in Action

Costco is another shining example of how integrity in pricing can lead to long-term success and customer loyalty. Unlike many retailers that constantly fluctuate prices based on market trends and profit margins, Costco adheres to a strict policy of charging a flat margin — no more than 14% — on all its products. This approach is not only rare in the retail world but also serves as a testament to Costco’s commitment to delivering value to its members.

What sets Costco apart is its unwavering commitment to passing savings directly to consumers. Even when the company negotiates lower prices with its vendors, those savings are immediately reflected on the shelves. This policy of transparency and fairness has cultivated a deep trust between Costco and its customers, who know they are always getting the best possible deal.

As Charlie Munger, a long-time advocate of Costco’s business model, has pointed out, Costco’s success is not merely the result of a good idea — it’s the outcome of decades of disciplined execution. Munger has often emphasized that Costco’s ability to maintain this level of integrity over time is what truly sets it apart. The company’s dedication to its customers isn’t just a business strategy; it’s a cultural commitment that permeates every aspect of its operations. By consistently delivering value, Costco has built an empire founded on trust — a rare commodity in today’s market-driven economy.

Realigning Incentives: A Path Forward

To create a more sustainable and equitable financial ecosystem, we need a fundamental shift in how financial institutions and crypto exchanges operate:

- Long-Term Value Creation and Ethical Innovation: Institutions should focus on creating long-term value for customers and developing new products that genuinely address customer needs, rather than just boosting short-term profits.

- Transparent Fee Structures: Implement clear, fair, and justifiable fee structures that align with the value provided to customers.

- Education and Empowerment: Invest in financial literacy programs and provide tools that empower customers to make informed decisions.

- Stakeholder Capitalism and Regulatory Collaboration: Adopt a model that considers the interests of all stakeholders — customers, employees, communities, and shareholders — and work proactively with regulators to create consumer-protective frameworks without stifling innovation.

Conclusion

The current misalignment between the incentives of financial institutions and crypto exchanges and the values of their customers is unsustainable. It’s time for a paradigm shift that places customer value at the center of the financial ecosystem. By realigning incentives, we can build a more trustworthy, stable, and inclusive financial future.

But this transformation won’t be easy. It requires a concerted effort from consumers to demand better and from industry leaders to pioneer this change. Only by working together can we create a financial system that truly serves everyone’s interests — not just those of shareholders.

As we move forward, the challenge is clear: How can we ensure that the pursuit of profit doesn’t come at the expense of consumer trust? And what role will you play in this transformation?

Written by

Kevin Hoang

.jpg)

.jpg)